Fixed Mobile Substitution (FMS) is the concept of replacing fixed telecommunications lines with mobile technologies.

In New Zealand the number of fixed lines in use has remained steady from 2006-2011. In Europe over the same period, the number of households without fixed lines increased from 18% to 27%. At the same time, penetration of broadband has increased in both markets.

High prices for data have kept New Zealand tied to its landlines for data while many Europeans have made the leap to all-mobile.

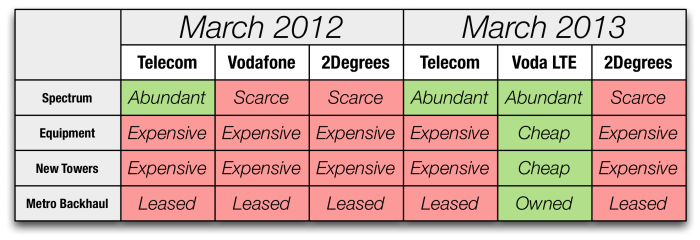

In support of high prices, New Zealand carriers have argued that spectrum is scarce, cellular equipment is expensive, and the cost of building towers is prohibitively expensive due to local councils and the Resource Management Act. As of this time last year all three carriers had the added operational expense of leasing fibre or Ethernet services to their towers for backhaul. These barriers have added up to networks that are generally running at capacity, with only high data costs to prevent users from overloading the network as in the case of Vodafone Australia.

All this changed in 2012 when Vodafone NZ made two strategic acquisitions. In May they performed a spectrum swap with CallPlus, converting what had been a fairly useless block of radio spectrum in to one compatible with a common variant of LTE. In October, the Commerce Commission approved their purchase of fixed-line carrier TelstraClear.

The TelstraClear purchase, in addition to bringing along a pile of radio spectrum, positions Vodafone as the only cellular carrier with their own metro fibre network. Vodafone has the added bonus of dense suburban reticulation through Christchurch and Wellington, in place to provide TV and broadband over a Hybrid Fibre Coax (HFC) system.

With metro fibre across most of New Zealand’s population and a new LTE network, Vodafone is positioned to be a strong competitor to UFB already. Their new LTE service using existing infrastructure is already twice the speed of the basic 30mbps UFB offering, but data pricing is being kept high to ward off network slowdowns. With a new fibre network and 2.6GHz spectrum, they could massively increase their network capacity without expensive equipment, tower builds, compliance costs, or backhaul OpEx using outdoor picocells. For example:

- Alcatel-Lucent’s MetroCell: A laptop-sized cell site designed to mount to a utility pole, requiring only 45 watts of power and IP backhaul and requiring no resource consent.

- Alcatel-Lucent’s LightRadio: A distributed cellular architecture for 3G and LTE comprised of tiny, fibre backhauled cubes that are spread throughout an area on utility poles. They’re usable alone for low densities of users and stackable for higher densities.

- Ericsson’s Bel-Air LTE Picocell: A laptop-sized LTE cell site that hangs from the same overhead coax lines that are used to provide cable TV – taking its power from the existing TV distribution network and using existing Ethernet services for backhaul.

All three can add an LTE sector of capacity to Vodafone’s network for less than $10k without new consents, tower leases, or backhaul costs. The Ericsson option could be rolled out to tens of thousands of customers in a matter of weeks. The combination of abundant spectrum, the ability to use cheap equipment, inexpensive or free access to utility poles as towers, and own-network metro backhaul are unique amongst New Zealand carriers.

Using LTE picocells to provide increased network capacity, Vodafone could easily offer products in to the market with UFB equivalent speeds – without any of the startup costs or long-term contracts required for fibre installations. Given the savings over paying an LFC $37.50/month for a UFB circuit, shifting just 5% of the fixed broadband market on to an LTE solution could add an extra $26M p.a. to Vodafone’s bottom line.

LTE Picocells + New Spectrum + Metro Networks could be a quick win Vodafone, who now have the option of providing a “Fibre Killer” solution.